Stephen W. Campbell earned a doctorate in history from the University of California, Santa Barbara, in 2013. A lecturer at California State Polytechnic University, Pomona, Campbell is the author of articles that have appeared in American Nineteenth Century History, Ohio Valley History, Perspectives on History, and History News Network. He has recently completed a book manuscript entitled Banking on the Press: Newspapers, Financial Institutions, and the Post Office in Jacksonian America, 1828-1834.

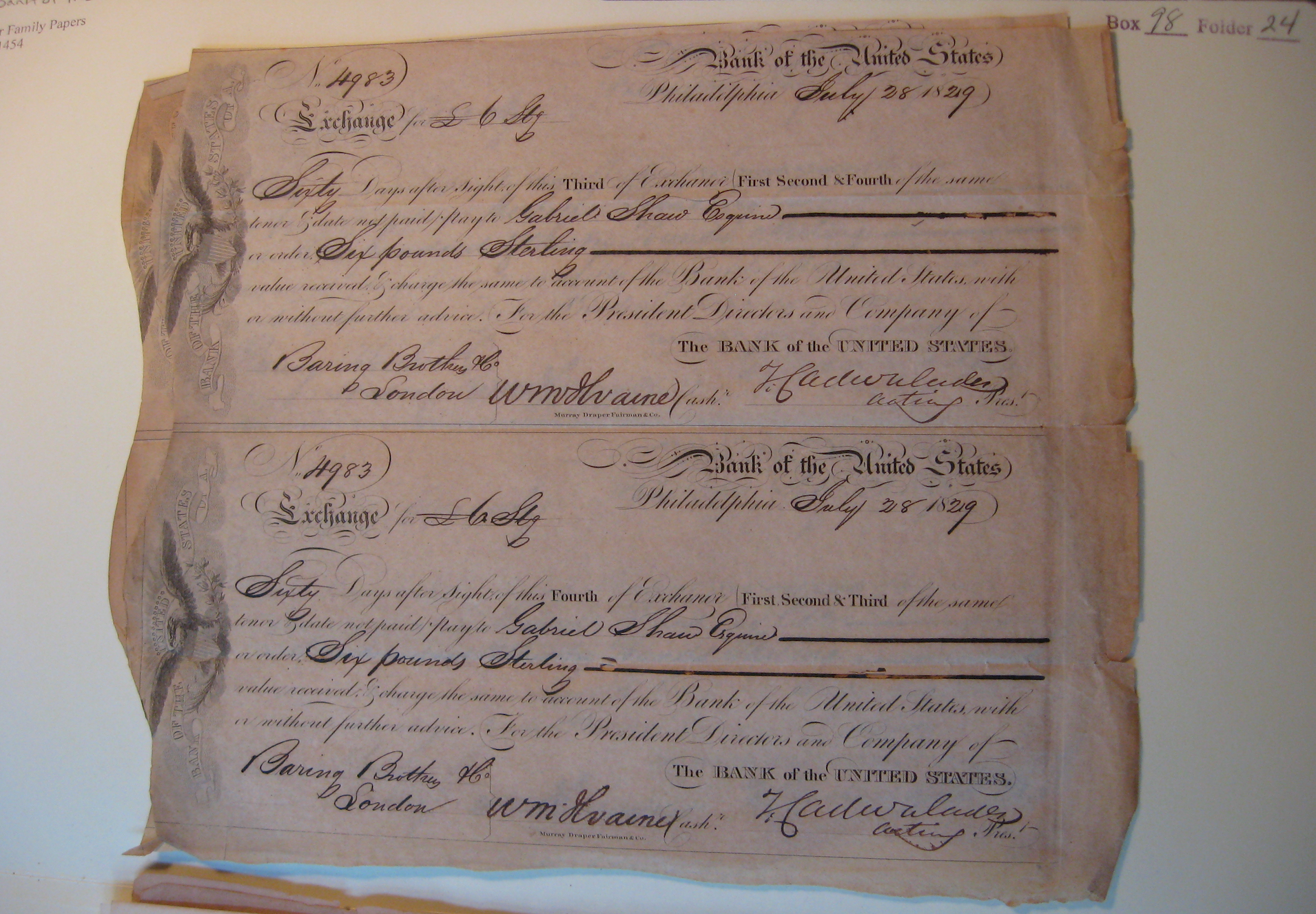

Cadwalder Family Papers, Box 98, Folder 24, Historical Society of Pennsylvania, Philadelphia, PA. [Click for full-size]

Unexpected “ah-hah!” moments make long hours of historical research worthwhile. A few months ago I was perusing a letter from an edited volume of Henry Clay’s correspondence when my eyes began to drift over to an adjoining page. A letter, dated August 17, 1830, showed the great senator and orator instructing his Washington agent, Philip Fendall, to send one of his slaves, Lotty, back to Kentucky. Clay wanted Lotty “to have the means to bring herself home…but if she wants money for that purpose I will thank you to apply to Mr. R[ichard] Smith to advance her the necessary sum.” Nothing in the footnotes or index shed light on this enigmatic Smith (an exceedingly common name both then and now), but I had come across this name several times before. This was almost certainly the cashier of the Washington branch of the Second Bank of the United States (BUS), the nation’s de facto central bank. A few weeks later, Clay again penned Fendall: “There are persons frequently bringing slaves from the district [of Columbia] to this State, some of whom might perhaps undertake to conduct [Lotty] to Maysville, Louisville, Lexington, or some other point from which I could receive her.”[1]

Sympathy would be the natural and appropriate response for a historian first learning about Lotty, a slave who at a moment’s notice could be forcibly removed across the country as if she was a pawn on a chessboard due to the cold calculations of powerful men like Clay and larger, impersonal forces far greater in strength than any individual’s ability to control, but for the purposes of my research, Clay’s letters generated excitement because they pointed to a seldom-discussed topic: the Bank’s involvement in the domestic slave trade. In the past two decades historians like Ed Baptist and Sven Beckert have located this trade within long-term patterns of American and global history through their pioneering work in the history of capitalism sub-field.[2] Baptist’s The Half Has Never Been Told caused quite a stir in the profession, leading to several spirited discussions at The Junto and even the retraction of a critical review written in The Economist. Employing penetrating class-based analysis in his examination of southern politics and economic growth in the 1830s, Baptist linked the BUS to a modernizing world of cotton and slaves. And yet, many of the specific mechanisms in which the BUS fueled slavery’s expansion remain opaque.[3]

Knowing the intricacies of Anglo-American trade can help us. Much like the famous merchant banking houses, Baring Brothers and Brown Brothers, which Baptist, Beckert, and others have skillfully surveyed, the BUS leveraged its status as a major player in global trade to finance the South’s slave economy. In the 1820s, British investors started purchasing large quantities of American securities—the stocks and bonds that capitalized banks, internal improvements, and state and municipal governments—in London money markets. Typically the BUS would sell U.S. treasury bonds to Thomas Biddle & Company, a brokerage firm headed by Nicholas’s cousin that had significant investments in Kentucky hemp growers and southern state banks that collateralized slave assets, which then resold the bonds to Barings.[4] British investors eagerly purchased American securities, in part, because of the value of slave-grown cotton exports. To set all of this trans-oceanic trade in motion, merchants employed a credit instrument known as a bill of exchange, a short-term (60-90 days), interest-bearing order that represented the value of cotton shipments. When a merchant presented a bill at a BUS branch office, the BUS purchased the bill and issued its own notes in return, allowing merchants and planters to receive immediate payment long before the cotton arrived in England.

Any examination of the few extant BUS balance sheets will show that most of the institution’s capital was in the North while its notes and bills were disproportionately concentrated in the South. For the year 1833, all of the Bank’s branch offices purchased a total of $67.5 million in bills of exchange. $46.3 million (68.6%) were purchased at branch offices located in slave states.[5] In February 1832, more than two out of every three BUS notes (67.9%) were issued here. If we combine the assets and liabilities from all of the BUS branches in the slave states and compare them with those of the region’s state banks (excluding other financial institutions), we see that nearly one out of every two bank notes (49.3%) in the slave states came from a BUS branch. Considering these figures, it is hard to imagine how the Bank could not have aided the expansion of slavery in some form or another. The planters, merchants, and brokers who bought and sold land, cotton, and slaves in a rapidly expanding economy required a circulating medium, which the Bank provided.

The BUS-slavery connections do not end there. Isaac Franklin of Franklin & Armfeld, the nation’s largest slave-trading firm, noted that the BUS was one financial intermediary that kept slave prices stable.[6] In addition, the BUS, according to its charter, could “purchase, receive, possess, enjoy, and retain… lands, rents, tenements, hereditaments, goods, chattels and effects [author’s emphasis]” not exceeding $55 million.[7] “Chattels” could refer to any number of personal possessions, but it is worth pointing out that corporations like the BUS often acquired slaves during the process of bankruptcy and debt liquidation. For this reason, the BUS, reconstituted as a private institution in 1836, eventually became one of the largest owners of plantations, slaves, and slave-grown products in Mississippi.[8]

The BUS ordinarily makes a requisite cameo appearance in the standard, survey-level US history textbook as a combatant in Andrew Jackson’s “Bank War.” In thinking about new ways to introduce students to this “peculiar” financial institution, the history of capitalism sub-field may be a guide. Knowing how credit instruments worked can help us place the BUS alongside Barings, Brown, and Franklin & Armfeld as a powerful financial engine in the Atlantic economy that mobilized northern and British capital to enable and profit from the domestic slave trade.

____________________

[1] Clay to Fendall, August 17 and September 10, 1830, in Robert Seager II and Melba Porter Hay, eds., The Papers of Henry Clay Volume 8: Candidate, Compromiser, Whig 1829-1835 (University of Kentucky Press, 1984), 253-4; 261-2.

[2] Edward L. Baptist, The Half Has Never Been Told: Slavery and the Making of Capitalism (Basic Books, 2014), xviii; 112-22; Sven Beckert, Empire of Cotton: A Global History (Alfred A. Knopf, 2014), xiv-xv.

[3] The near absence of any sustained, detailed analysis of the Bank’s relationship with slavery is a result, in my mind, of at least three factors. One, Nicholas Biddle, in 1841, destroyed much of the Bank’s official business records, leaving historians to rely on the financial statements within Biddle’s correspondence and miscellaneous sources and manuscript collections scattered throughout archives in the United States to reconstruct how the BUS worked. Two, almost all of the monographs on the BUS were published before 1975, when our knowledge of the domestic slave trade was more limited. And finally, while not insurmountable, the domestic slave trade has always posed challenges to researchers because many actors involved in the trade deliberately concealed the nature of their work. While I have critiques of his book, one exception to this trend is Richard Holcombe Kilbourne, Jr., Slave Agriculture and Financial Markets in Antebellum America: The Bank of the United States in Mississippi, 1831-1852 (London: Pickering and Chatto, 2006).

[4] AJ Alexander to Thomas Biddle, May 4, 1831 and April 10, 1832; John G. Gamble to Thomas Biddle, April 10, 1833, Thomas Biddle Correspondence, Historical Society of Pennsylvania, Philadelphia.

[5] Niles’ Weekly Register, June 1, 1833. Calculations performed by author.

[6] Isaac Franklin to Rice Ballard, June 8, 1832, Rice Ballard Papers, Southern Historical Collection, University of North Carolina, Chapel Hill.

[7] Annals of Congress, House, 14th Congress, 1st Session, Appendix, 1815-1816.

[8] Kilbourne, Slave Agriculture and Financial Markets in Antebellum America, 2.

This is a fascinating piece Ben. I am looking forward to where this discussion leads. The connection between the BUS and the domestic slave trade raises questions in my mind concerning the ideology and influence of anti-bank Americans. If northern financiers and the BUS were providing the crucial capital for the expansion of the domestic slave market, why did so many anti-banking voices come from slave-holding states and salve owners, such as Jackson himself?

The connections between the BUS and the domestic slave economy demonstrate a much greater entanglement of the BUS with a variety of historical problems of the early US. The competing interests and platforms of anti-bank and pro-slavery Americans would seem to make the anti-bank politics of the 1820s and 1830s much more complicated than previously thought.

Thanks for your comment! Indeed, as you say, this is a complex topic and in a 1,000-word piece, I can only address so much. I develop some of these thoughts more deeply in what I hope will become a book chapter….If the Bank was so valuable to the South, then, why did so many southerners oppose it? The politicians and constituencies who joined Jackson in defeating the Bank, the regions they inhabited, the occupations they held, and their reasons for opposing the Bank have been the subject of a vast historiography that goes back decades. Perhaps historians need to take seriously southerners’ constitutional scruples about a federally-chartered corporation. Perhaps what seems like a fairly clear case of rational, economic self-interest to modern readers—a southerner supporting the Bank—may not have been so rational for people living in a different cultural milieu, operating with different assumptions. What is rational is ultimately subjective, constructed, and changes over time. Opposition to the BUS in the South might be an apt illustration of how personality, psychology, identity, nostalgia, nationalism, and what Keynes called “animal spirits” so often seem to triumph over pure pocketbook politics. Jacksonians had a head start in party organization over their opponents and the Jeffersonian suspicion of concentrated financial power may have had true staying power in the South. If the testimony presented in Clayton’s investigation is any indication, the processes through which the Bank financed the South’s economy were highly technical, arcane, abstract, and complex, making it difficult for the layperson to understand. The Bank’s regulatory and financial benefits may have been like health insurance in modern America: one does not realize its value until it is gone. Any and all of these issues could be true, including the ones that have not been mentioned.

A few other points…One reason that commonly appears in the historiographical literature is the jealousy of state banks who desired the national Bank’s public deposits, monopolistic relationship with the federal government, and ability to lend at low rates. While this may have been true in New York, Georgia, and a few other areas, my own research suggests that there are many reasons to be skeptical of this viewpoint (or at least recognize that it is one issue explaining opposition to the BUS, but by no means the only one). The national Bank rescued state banks from collapsing on more than occasion. And during the years when the Second Bank acted like a central bank, the institution pursued regulatory policies that were beneficial for state banks; namely in preventing over-lending. In addition, there were many instances in which the national Bank and state banks performed different types of financial services, meaning they were not in direct competition. Baptist writes that the BUS-planter alliance angered non-slaveholding whites in the South, Jackson’s most ardent supporters. The yeomen, the story goes, wanted more easy credit. I think this is certainly *part* of the discussion, but I would like to see more evidence of it before I accept it as a central explanation of white southerners’ attitudes toward the BUS.

Pingback: New York History Around The Web This Week | The New York History Blog